Over the last years, the liquor industry in Australia has experienced one of the most tumultuous periods in living memory. From the pandemic and cost-of-living pressures to consumer trends around moderation and sustainability, various factors have impacted behaviours, consumption, and spending. Further complicated for liquor manufacturers and brand owners by the fragmented nature and gaps in consumer, shopper, and category data available in Australia.

Higher cost-of-living impacts on-premise traffic

With the cost-of-living pressures, it’s no surprise that consumers have been taken some strategies to manage their expenses, such as becoming more home-centric and going out less, leading to a reduction in visits to bars and restaurants. CGA’s Pulse+ report indicates a 2-percentage point drop in the on-premise consumer penetration for July compared to the previous year. Frequency has also been dropping, with 39% of consumers claiming they are going out less than usual (compared to 24% going out more and 37% going out the same as usual).

As expected, these penetration and frequency reductions bring challenges for on-premise performance, leading to a contraction of -7.7% in total spirits volumes. This is in contrast to beer’s 1.4% volume growth compared to the previous year, suggesting that spirits are more impacted by factors such as price increases and perceived value for money.

However, this situation is not all negative for liquor brands and retailers, as consumers are replacing out-of-home occasions with drinking at home. When it comes to in-home drinking, off-premise unit sales stable, but value growing compared to the previous year. Although units per occasion has decreased by -3.3%, there’s an uptick in both buyers (+2.1%) and occasions per buyer (+1.7%), suggesting that people might be shifting some occasions to at-home consumption but also purchasing smaller pack sizes more frequently, indicating a move towards occasion-based buying rather than stocking up. Similar to the On-Premise channel, beer is the primary beneficiary of value-driven consumer mindsets, facing double-digit dollar value growth through increased buyers and occasions per buyer, benefiting from the consumer shift towards Off-Premise drinking.

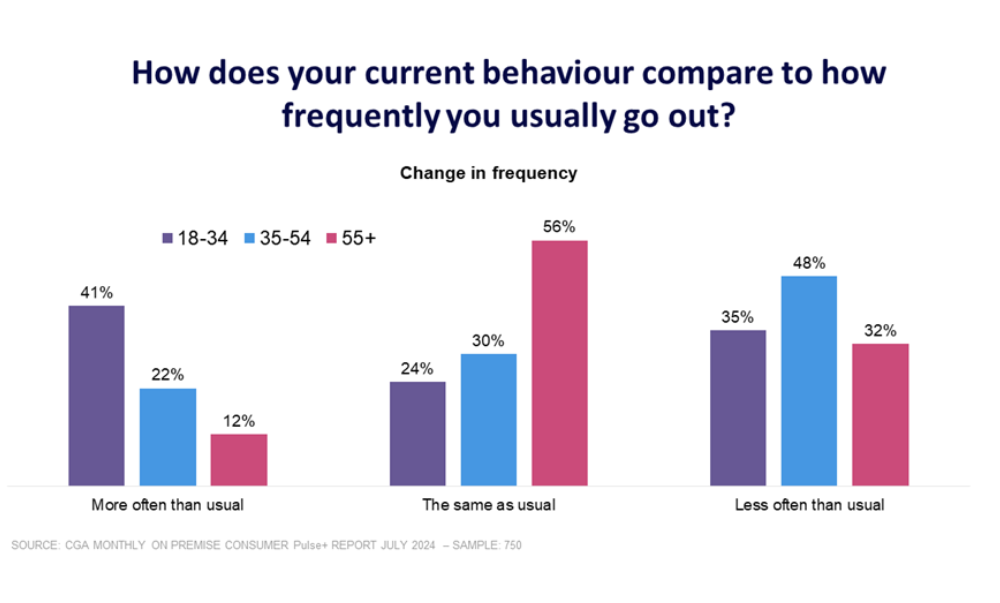

Different occasions, different demographics

Despite the high cost-of-living context, not all consumers are reducing their on-premise visits equally. Young consumers (18-34 years old) are visiting pubs, bars and restaurants more often than before, but on the other hand, middle-age consumers (35-54), more likely to be paying mortgages and raising children, are the ones usually going out less often. Comparatively, off-premise data (NIQ’s Omnishopper) shows that older consumers (55+) show the strongest increase in liquor retail sales growth (34.1% value growth compared to the previous year), while under 35s show the biggest reduction in retail spending on total liquor (-8.0%). Declines for under 35s are driven by decreases in buyers and occasions per buyer, potentially as people counteract the effects of the cost-of-living crisis by stopping their at-home drinking or reducing occasions to prioritise experiences and consumption in the on-premise. In addition to that, this could also reflect moderation trends manifesting as abstinence among these consumers.

Comparatively, off-premise data (NIQ’s Omnishopper) shows that older consumers (55+) show the strongest increase in liquor retail sales growth (34.1% value growth compared to the previous year), while under 35s show the biggest reduction in retail spending on total liquor (-8.0%). Declines for under 35s are driven by decreases in buyers and occasions per buyer, potentially as people counteract the effects of the cost-of-living crisis by stopping their at-home drinking or reducing occasions to prioritise experiences and consumption in the on-premise. In addition to that, this could also reflect moderation trends manifesting as abstinence among these consumers.

What are the main reasons driving consumers to still go out? Special/Event-based occasions (i.e.: celebrations, live sports and music, etc) are still a good reason for having drinks at bars and restaurants, growing share of occasions from 33% to 38% compared to the previous year, at the expense of traditional food-led (from 36% to 33%) and drink-led (from 31% to 29%), according to the latest OPUS report (On Premise User Study).

Diving a bit deeper, we can see that demographic differences play a key role in on-premise consumer occasions and categories, and helps to understand why young consumers are still going out. Gen Z (40% share of all occasions) and Millennials (41%) prioritise these experiential occasions more than Gen X (36%) and Boomers (32%). In line with their quest for experiences, we also note the high proportion of these younger consumers who prefer different drinks at bars/restaurants compared to home. This suggests that on-premise consumption/visitation plays a more unique and differentiated role in their lives than it does for older consumers, making it less replicable at home and could be one of the reasons why many young consumers are either going out as much as before or even more often despite the higher cost-of-living.

With the on/off role continuing to evolve, the need to measure it ongoing is clear, drinks suppliers in Australia are already reaping the benefits of our NIQ Full View.

Chris O’Shea, Head of Category at Brown-Forman, said: Having a partner with expertise and solutions across both on and off Premise channels is invaluable, as it allows us to holistically view the changing drivers, behaviours and trends flowing between the two channels, and strategise on how to maximise our success."

"The team at NIQ are always responsive, knowledgeable, and go above and beyond to ensure we’re getting the most out of our subscription. We truly value this partnership and look forward to continued success together," added O'Shea.

Article contributors: Marco Silva, Customer Success Director, NIQ; Luisa Correa, Customer Success Manager, NIQ; and Thomas Graham, Senior Customer Success Manager, NIQ

NIQ is a Platinum Partner of the Drinks Association.